Front and center industry analyst disclosures: Your trust is important to us, as such, we strive to disclose our client relationships, some which are listed in the following post, read Altimeter’s disclosures page.

Research Summary: Growth in Vendors and Market Demand –Yet Space Is Immature

Social Media Management Systems, like CMS systems for websites, these SMMS systems (see list of all vendors) help companies manage, maintain, and measure thousands of social media accounts, are the next growth market for the social business category. While saturation is at 58% of corporate buyers, the average deal size is a meager $22,000 but will expect to grow to six figure annual deals in coming quarters to meet market demand. This growing space has low barriers to entry, which result in a flood of clones, but expect only a handful to remain after a shakeout to serve enterprise-class buyers. Buyers and investors should focus on vendors that understand business –not just technology, offer services and reliable SLA, and deep integration with other social systems. In the future, this technology set will mature to grow into a data company that will extend it’s scope beyond simple Facebook and Twitter and impact how marketers approach the market, product innovation, and supply chain.

[Although the nascent Social Media Management System space is only one year old, 58% of corporations have adopted at least one of these 28 vendors]

Altimeter is conducting a formal research report on the SMMS topic (see research agenda for 2011), However, I wanted to give a year end state, after coining this category 12 months ago and listing out vendors, read the List of Social Media Management Systems

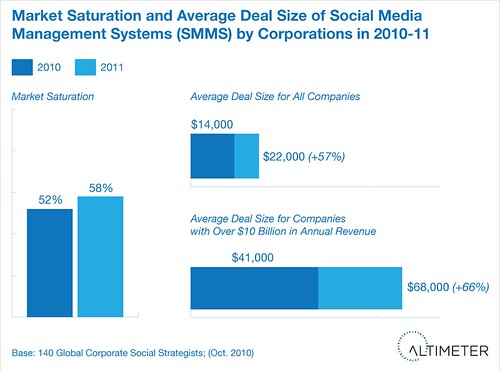

Above Graphic: Market Saturation and Average Deal Size of the Social Media Management Systems (SMMS) by Corporate Buyers in 2010-2011

Year One in Review: New Entrants, Acquisitions, and Growing Deal Sizes.

Just a year ago, we saw the rise of the new category Social Media Management Systems, (I must give credit to Cisco’s Social Strategist LaSandra Brill for giving me the kick to start it). To understand the macro trends of this industry, read with the Social Business Stack, which shows SMMS as only a component of the overall purchase set for corporations. Here’s a breakdown of what’s occurred in the past 12 months:

SMMS By the Numbers:

- Growth rates rose 11% from corporate buyers. In 2010, adoption of SMMS systems by corporate buyers was already at the 52% and in 2011 buyers indicated they will be at the 58% adoption rate.

- Deal sizes grew 57% in last year. While there was significant relative increase in deal sizes the overall average annual deal size per corporate was $14,000 in 2010 and rose to $22,000 in 2011 according to our research of 140 corporate buyers.

- Large corporations spend $68,000 per year. For corporations with over $10 billion in revenues, the deal sizes ballooned to $68,000 per year on average, demonstrating that the larger corporations need these tools in order to manage their hundreds of accounts. (more data here)

- 65% Increase in vendors in last 12 months and growing. When I started this list, there was 15 vendors after launching the list after the first week. Today, the list has grown to 23 vendors (and I’m continuing to add vendors, with a market growth rate of 65% increase in new entrants, this will only continue this year.

- Growth markets in consumer facing and large corporations. While I noticed that Telecom and Tech were early adopters, I’m seeing growth opportunities in Retail, Hospitality, Restaurants, Consumer Tech, CPG, and all Regulated Industries.

- Consolidation: at least three acquisitions. CoTweet was recently acquired about a year ago by marketing platform ExactTarget, months later Objective Marketer was acquired by Email Vision, and just in this past Feb Constant Contact acquired SCRM company Bantam Live which has some SMMS features, all which are email/direct marketing solutions. Among all these acquisitions, we’re seeing these tools tie into greater marketing platforms for additional value.

- Some early forerunners –but don’t expect a clear winner. I’ll do more detailed analysis on these vendors later, but right now I’m hearing from buyers the following vendors: CoTweet, Hootsuite, Sprinklr, Spredfast and newer entrant Expion. Interestingly, former Community Platform vendor with enterprise experience Awareness Inc has double downed on this market and shifted away the saturated community platform market by launching Hub.

- Early vertical focuses have emerged and partnerships. We’ve already started to see verticals appear, such as GOSO for the Automotive dealer space, and expect this to continue in specific markets like hospitality, restaurants, travel, CPG, and Retail. Another new entrant was an entry by initially a consumer tool Seesmic, who received funding by Salesforce –the first enterprise vendor now with integration with social aggregation tool Chatter, and now Yammer. There was only misfire, as KeenKong changed their product strategy and never launched in this market.

Market Demand: Six Forces Spur On This New Category

There are a handful of forces that are increasing the demand for this year old category, among them (but not limited to) include:

1) Corporations Struggle to Manage Hundreds and Thousands of Accounts

The target market is hospitality, retail, and CPGs. Each of these corporations has dozens to hundreds of unique brands, and then regional rollouts. For example, some hotels could have up to 15 brands, and each having 4,000 hotel locations (half being distributed franchises), each with 10 social media accounts (there’s more to the social web that Facebook and Twitter, across a variety of languages. Furthermore, there’s high turnover in the localizes marketing and sales manager, who also lacks a background in online communications.2) Kenneth Cole and Chrysler Debacles Prove Need for Parental Controls

In the last few months, we’ve seen some severe examples of mis uses of corporate social accounts which could have been prevented by having a process and toolset to support (see the long list of “punkings“). In particular, Kenneth Cole’s ill-fated tweet tying the Egypt situation with spring sales was met with a riotous reaction, and last week’s Chrysler’s F-Bomb tweet resulted in firing of an entire agency. As a result, expect that many regulated companies will demand compliance regulations with social media, and be mandated to invest in SMMS systems to preview, flag, an process content before it’s published. Of course, this brings forth a few challenges such as less real-time approach, and a more sanitized corporate approach to discussions that will ultimately decrease credibility as authenticity may waver.3) Expect Regulatory Industries to Require This Safeguard System

Similar to the mess-ups listed above by Kenneth Cole and Chrysler will cause regulatory industries to give pause on how employees will use these technologies. As a result, expect healthcare, pharma, insurance, auto, finance and beyond to start looking at using these tools for all employees and even corporate accounts. Expect a keyword filtering system and workflow to be put in place to monitor then recommend a course-of-action to correct deviant tweets and Facebook messages. The downside? The rapid pace of the real world conversation will be slowed for many, but expect seasoned veterans to unleash the SMMS shackles for open conversations.4) Direct/Email Marketers Want a Piece of Social Marketing to Blast in New Channels

This toolset is an attractive addition to existing direct marketing platforms like email marketing suites that are used to publish thousands of emails to customers on a daily basis. Direct marketers, who want to get on the social bandwagon are finding religion and are now blasting content on social channels to networks comprised of news, deals, and offerings with mixed engagement and interaction.5) Agencies Know SMMS Provides Client Lock-in and Recurring Revenues

The social media service industry knows they must be value added beyond strategy and community management. They are seeking recurring revenues for accounts on a monthly basis in order to glean the hundreds of thousands per client, see data to learn more. By using SMMS systems, often coupled with brand monitoring and reporting services, they are now able to be full-service to listen, engage, and measure how companies are interacting with their customers on social channels. By partnering with SMMS systems some are white labeling the service, and using this in front of clients as a value added software, suggesting a perceived lock in with data and reporting –giving agencies the opportunity to become the Social Media Agency of Record (SMAoR).6) A Complementary Toolset for Social Platforms, Social Commerce, Brand Monitoring Vendors, Marketing Automation

First, understand how SMMS fits into the overall Social Business stack. You’ll notice it’s a sister technology to the technology “aggregation” displayed to the left of it. You’ll also notice that it’s below brand monitoring firms, and sits on top of Social Platform technologies. To the left of it you’ll find it is part of the data story in infrastructure and to the right of it services. Other places to watch for acquisitions will be social commerce platforms, as well as marketing automation platforms as they must spread into this space at a rapid pace to glean the revenues.

Predictions: Vendors Move-out-of-Garage to Meet Buyer Needs

These companies are young and early, and lack maturity like the established community platform space, here’s a few closing thoughts:

- This One-Year Old Space Shows Parallels to the 5 Year Old Community Platform Space Similar to how in 2007, how we saw trends for the Community Platform market, labeled it, and went on to research the space, I’m seeing similar trends (entrepreneur styles, deal sizes, market saturation) in this early SMMS market, just one year in.

- Vendors startup mentality clash with real buyers needs. Many of these garage startups lack understanding of corporate buyers. Not uncommon to seed, angel, and A round vendors, a majority of these vendors lack corporate buyer perspective. To learn more about the buyers of SMMS read the report about the Career Path of the Corporate Social Strategist.

- Vendors will finally offer and enterprise class service level agreements. Mainly focused on platform development, and also being discouraged by investors to add services to the mix, most of these vendors lack the staff to serve a corporate buyer who needs a high degree of hand holding in social business. Better yet, read Petra Neiger, one of Cisco’s Corporate Social Strategists perspective on what’s needed for buyers.

- Analytics and reporting to be a core focus on 2011-2012. These early platforms are focused on management of the social channels, and most do not have strong analytics and reporting technologies. Furthermore, they are often not connected to other reporting systems, and are data silos.

- Expect corporate adoption to reach 90% within three years . Expect market saturation to hit 90% range in three years, and average deal sizes to exceed $100k per year on average corporation –just as the Community Platform space have experienced over the past five years. Vendors that can align their product roadmap to the SMMS maturity roadmap stand to be one of the standing contenders.

- Deal sizes will reach six figures on average. I saw this trend before with the $25-50k deal sizes with community platforms about 5 years ago and have watched them balloon to $200k-300k for advanced and larger corporations on an annual basis. I expect similar patterns to emerge here as new functionality is offered and as the SMMS connects to other systems for lock in. Right now the average SMMS deal size is a mere $22k, yet as we segment out corporations with high revenues (over 10 billion, annually) they are already clinching $68,000 deal sizes –remember it’s only year one. Read more about how corporations should spend on social business.

- Market will reach over 100 vendors. Just like the crowded brand monitoring space (150 vendors) and community platform space (125+) vendors expect this category go balloon due to low barriers to entry, VC funding, and commodity technologies. In the long run, only a half of dozen will matter to the enterprise, as market consolidation will occur. Expect the 90+ that don’t become first of mind to corporate buyers to head into specific market verticals and SMB focus.

Well that’s my perspective after watching this space for the last 12 months, while I’ll continue to give updates, expect another wrap-up next March in 2012.

Update: This is cross-posted on RWW

Rayovac has found great success with Shoutlet. Shoutlet has kept pace with the ever evolving rules of social engagement and provided valuable guidance along the way.

Hey Jeremiah “ Fantastic insights as always.

I see Shoutlet has been mentioned a couple of times so I thought I™d weigh in.

We provide enterprise social management software for companies to build, manage, and measure their interactions on Facebook, Twitter, YouTube, and LinkedIn within one platform. Some differentiators for us include a true Social CRM for Facebook, Twitter, and YouTube; promotional widgets and a contest platform that utilizes HTML5 for mobile devices; Facebook eCommerce via our Shop & Share functionality; multiple brand/franchise/agent control through workflow management, administrative oversight, and permissions based accounting of all content; and customizable, real-time analytics that track user communication, who sees it, and where it’s shared.

I look forward to your thoughts about enterprise-level social management going forward.

David Prohaska

VP “ Marketing, Shoutlet

I’ve been using Spredfast for about a year, after evaluating some other tools like Sprinklr and Co-Tweet. Spredfast has better analytics, reaches more social destinations, and has better publication options. Their new release put on an awesome UI and their roadmap is to die for.

Perry Ellis International has been using Shoutlet for some time now. The platform offers up a variety of tools including social CRM, that have proven to help in our efforts to gain brand recognition across various social media sites. Aside from the new platform being user friendly, the team at Shoutlet has always gone above and beyond to assist our team.

Perry Ellis International has been using Shoutlet for some time now. The platform offers up a variety of tools including social CRM, that have proven to help in our efforts to gain brand recognition across various social media sites. Aside from the new platform being user friendly, the team at Shoutlet has always gone above and beyond to assist our team.

Thanks to Ragy Thomas and Sprinklr, DailyCandy has seen tremendous growth in our social presence / engagement – we love the workflow, analytics, and ability to identify and target our most influential followers!

Jeremiah- We (Socialware) are definitely seeing a lot of financial services firms tackle the issues that you address in #3, and there are options to do this without bogging down interaction times.

At Dell we use Sprinklr. While this field is still nascent, they get what corporations need to manage their social media presence. Still a long way to go, but we feel comfortable in their direction.

At Dell we use Sprinklr. While this field is still nascent, they get what corporations need to manage their social media presence. Still a long way to go, but we feel comfortable in their direction.

Great summary, Jeremiah. Feels to us at Spredfast that 2011 and beyond is going to be about company-wide social media management – more people involved, more activity and processes to manage and more to analyze. Let alone keep pace with the continued innovation coming from the social networks.

As with many enterprise platform markets, this should shift the conversation from WHAT specific features are present (most everyone will have the basics) to HOW well a platform helps people, groups and whole companies work better. Tons of things go into that – as you have noted – enterprise SLAs, scalable training/enablement, vertical orientation/content to accelerate adoption, user interfaces purpose built to support less sophisticated users, direct integration to existing communication processes. Good stuff. Things that help customers succeed with and prove the value of social communication on a broad scale.

Its going to be a fun year in this market.

BTW – you missed one other trend for this space in 2011 and beyond – SMMS providers will continue to be atrocious spellers.

Jim Rudden

CMO

Spredfast

@spredfast

For Starwoood Hotels & Resorts Worldwide, we have partnered with Buddy Media for more than 2 years to execute one of the largest social media executions known. With 9 Global Brands and more than 1,000 of our properties now having FaceBook Fan Pages, we have been able to seamlessly engineer a massive social engagement tool for our business. Buddy was the only platform that could provide us with the scalability and seamless content distribution mechanisms to allow us to administer such a program. We looked at many of the other platforms mentioned here and ultimately settled on Buddy for their strategic leadership relative to social management and frankly their willingness to address our needs as we have grown.

For SMBs, today™s focus is figuring out what social media marketing is and, more specifically, how to put social media marketing to work. Once the right program for a business is up and running, additional value will come from being able to effectively track and manage conversations and activities across multiple channels, including Facebook, Twitter, and traditional email. Some will use all online tools, but others may only tune in to specific social outlets. A consolidated view will give businesses the visibility and insight they need to engage with their contacts effectively and efficiently.

For SMBs, today’s focus is figuring out what social media marketing is and, more specifically, how to put social media marketing to “work.” Once the right program for a business is up and running, additional value will come from being able to effectively track and manage conversations and activities across multiple channels, including Facebook, Twitter, and traditional email. Some will use all online tools, but others may only tune in to specific social outlets. A consolidated view will give businesses the visibility and insight they need to engage with their contacts effectively and efficiently.

Eric Groves

Senior Vice President, Global Market Development

Constant Contact

We’ve worked with Buddy Media for over a year to help maximize our brand presence on Facebook. Through building tabs utilizing their Drag-and-drop Facebook Page builders, we have been able to engage fans with our content and easily update this content to continue to drive interaction. Using their wall publishing tool has enabled us plan and pre-scheduling our posts and easily track the interaction with these post, helping us to better understand what content is engaging. We™ve been able to save time and effort moderating our page by setting up notifications, alerting us to new engagements that may require us to take action. Most recently we™ve launched an exciting new application with Buddy Media that allows our clients (hair salons and stylists) to integrate our brand content on their own business Facebook pages, increasing our digital impressions to a very targeted audience, their clients and their clients friends.

Great article, Jeremiah.

Although you touched on it, a major trend we are seeing at Sendible.con is the demand for agencies wanting to offer a White labeled version of our platform to their clients. Sendible is a social media management platform that incorporates social media, email and SMS marketing into a single tool for SMEs. It would be great if you could include our product in your list of SMMs.

Same here – we adore Shoutlet! It’s so incredibly easy to use and their clear focus on UX and solid functionality over extraneous (read: not useful) bells & whistles really shows in the end product. Every time I log in I feel like I’m playing with the shiniest, coolest, most amazing toy — with the awesome side benefit of driving real and quantifiable business value for us.

You have stated:

“Just like the crowded brand monitoring space (150 vendors) and community platform space (125+) vendors expect… ”

Could you post those lists (for both monitoring and community)?

I understand this is an old post, but I thought would be nice to see the 2011 list, so we can compare to 2012.

Thank you for the great post!

Alex

You have stated:

“Just like the crowded brand monitoring space (150 vendors) and community platform space (125+) vendors expect… ”

Could you post those lists (for both monitoring and community)?

I understand this is an old post, but I thought would be nice to see the 2011 list, so we can compare to 2012.

Thank you for the great post!

Alex

Great piece of research on SMMS Jeremiah! – Is there any update for 2015? How has your forseen market consolidation in your opinion impacted small vendors in the space? Who are the winners and losers?