Executive Summary

Research has found that out of 55 Social Business Startups that a majority (69%) have received early and late stage funding, averaging $14m in total funding. A significant 31% have not taken investor funding, which we’ve listed 6 reasons ranging low costs of operations, self-funding, VC avoidance, and market saturation of startups. 18% of startups had achieved a material event (acquired or IPO) and of them, 40% we’re not funded. Expect three macro trends in 2013 including: 1) Startups focus on business value to battle software giants, 2) Investors hot on SMMS market, but wary of vendors who lack differentiation, and 3) As Social Business Software market matures, expect growth in late stage investments

Research Background

I’m continuing industry analysis of Social Business Software funding and will do a series of data cuts from my sample of 55 software vendors to tease apart trends, insights, and built a forecast for what is to come. First, read part one on The State of Social Business Software (including methodology of this study), which dissects into funding amounts, averages, and frequency of funding rounds. I interact with VCs, startup entrepreneurs, software giants, brand buyers, press and media to obtain multiple points of view.

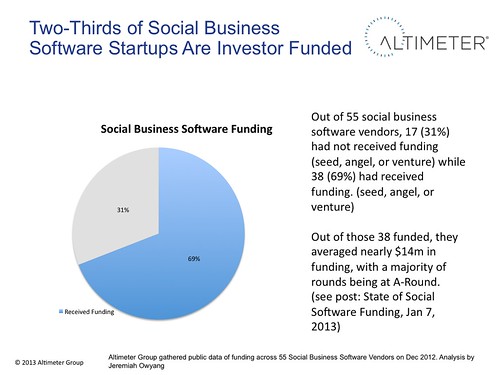

Above: Figure indicates that while two-thirds were funded, a large set of social business software vendors were not funded, a rate greater than I expected to see.

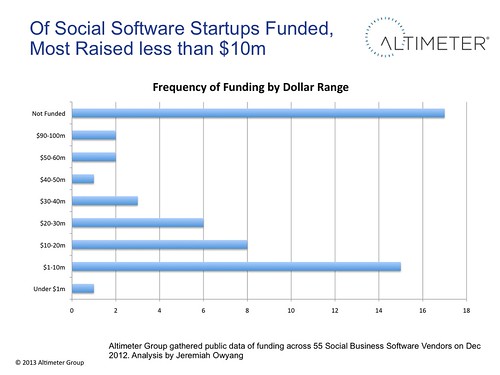

Above: Of the two-thirds who were funded, a majority of them raised a small amount of money, most commonly under $10m, a paltry amount compared to funding rounds in other tech categories in prior decades.

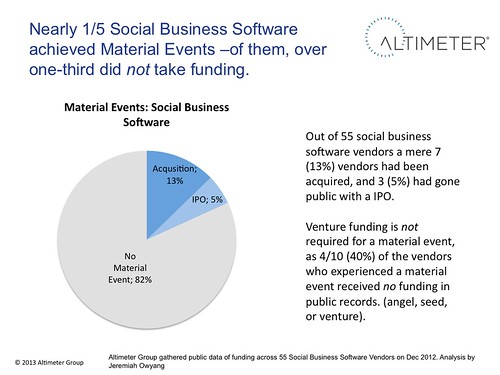

Above: The industry ratio of 18% of startups achieve a material event, still holds as an industry benchmark. I found that consumer based startups may have a lower rate of material event, but with larger returns. Interestingly, 40% of those who achieved a material had no public records of funding from angel, seed, or venture investors.

Key Data Points

After cutting/comparing/probing this data sample of Social Business Startups (not consumer startups like Facebook, Instagram, Twitter) the following data points were discovered:

- A total of 55 Social Business Software Vendors were selected for this sample set.

- 17 (31%) did not take funding per our searchers on public websites, press releases, S-1 filings and Crunchbase.

- 38 (or 69%) were funded in public records listed as Angel, Seed, or various Venture Rounds

- Of the 55 startups, 17 we’re not funded, and the majority who we’re funded (16) received less than $10m in total funding

- 7 startups were acquired by larger corporations (Buddy Media/Radian6 to Salesforce, Context Optional to Adobe, Viture/Involver to Oracle, etc)

- 3 startups achieved IPO (Liveworld, Bazaarvoice, Jive)

- A total of 10/55 (18%) of startups have achieved a material event.

- 6/10 (60%) of the startups who achieved a material event (IPO, Acquired) were funded.

- Of the 6 startups who achieved a material event, they averaged total funding amount of $26.3 million.

- Of the 6 startups who achieved a material event, the largest round raised was Buddy Media’s D-Round at $54 million.

Material Events, defined, debated.

For the purposes of this report I’m defining a material event such as an acquisition by another company or IPO for publicly traded shares. There have been many arguments made that successful companies do not need a material events, if they can yield consistent dividends to investors. The challenge is that the venture model requires multiples returned per fund to LPs in order to raise monies for future funds. VCs tell me “You’re only as good as your last fund” and with fund management being 5-10 years, there’s a time clock on returns, causing pressure on executive teams to achieve a material event. It’s also worth noting that in some cases, an acqusition occurs because a company is distressed and is auctioned as a fire sale.

Nearly One-Third of Startups Avoided Funding

While over 2/3rds of startups took funding, a surprising 17 (31%) did not take funding in the form of seed, angel, or venture funding (A, B, C, D, rounds). This number is shockingly high, as in previous decades tech startups were dependent on Sand Hill investors to anoint companies to market. Today’s market has changed and startups are not dependent on VCs. Even of those who achieved a material event, 4/10 (40%) did not have funding. There are six primary drivers why entrepreneurs have confided in my why they don’t take funding

In near future, I’ll post why 60% of startups prefer funding, surprisingly, it’s not just about the money.

| Reason | Description | What Entrepreneurs Don’t Tell Anyone |

| 1) Self Funded | In most cases where I see self-funded startups, often the executive team are self-funding from prior wins as a serial entrepreneur. | This means more money for them, control. In some cases, the serial entrepreneurs I’ve met are doing this company both for personal accomplishment, fun, and are no longer driven by monetary gain alone. |

| 2) Company Too Early Stage | A large portion of startups in our sample set were early stage, (many in SMMS market) who do not yet need expansion and growth funds. | In some of these crowded markets, they’re struggling to get favorable terms as first time entrepreneurs, slow growth, or in a crowded market. |

| 3) Low Costs to Start Company | Today’s startup needs a few 10’s of thousands of dollars to get going, with recurring SaaS licence revenues, they can sustain after one year of landing a few key brands. | Cloud technologies, open source, virtual workforces, and overseas developers make today’s startup a low cost. |

| 4) Seek Lifestyle Company | Often a controversial discussion in tech circles, many entrepreneurs want to avoid pressures of a material event put on them by investors | Being an entrepreneur is tough work, when your company does well, the board may want the founder out, requiring them to go to beach get board, and get itch to restart. An addictive, never ending cycle. |

| 5) VC Avoidance | Unfavorable terms, pushy board members, or lack of value-add cause entrepreneurs to shudder. Additionally, the time required to pitch, negotiate, expose secret plans, and deal with new influencers on board a risk if they don’t see eye-to-eye. | Many serial entrepreneurs confide that they’ve been burned by VCs in the past, and as a result seek to avoid them as long as possible. |

| 6) The Startup is a Bust | Some startups are clones, unoriginal, and will not succeed and VCs simply know a failure when they see it. In fact, we track 28 SMMS vendors in the active market. | Entrepreneurs are prone to bluntly admitting this. Instead, expect euphemisms such as “strategic roadmap pivot to respond to changing market conditions”. ahem. |

Market Trends: 2013 Social Business Software and Funding

Expect three macro trends in 2013 when it comes to social business software, their buyers, investors and last year’s activity, they include:

- Startups focus on business value to battle software giants. Have At the high level, social business startups must focus on value creation and market domination as after the rash of M&A in 2012 (Adobe, Oracle, Salesforce, Google), this has left an opening for independents to build value while blue chip software companies re-tool and figure out their suite strategy up until the second half of 2013. With the IPO exit taking a major beating from Facebook, Groupon, Zynga, and questionable results from Bazaarvoice, social business startups must focus on recurring revenues through business value to clients.

- Investors hot on SMMS market, but wary of vendors who lack differentiation. While the brand monitoring, community platform, ratings and reviews space has already consolidated, VCs look at SMMS market, despite a handful of acquisitions. My time on Sand Hill road has yielded excitement and hesitation from VCs examining the fast growing –yet crowded– social media management systems space. Expect SMMS vendors who can achieve market differentiation and integration with larger blue chip software players to be ideal for investor funding –our findings indicate the market is not strong at differentiation.

- As Social Business Software market matures, expect growth in late stage investments. There’s room for independent players who’ve not yet been acquired to land and expand their enterprise clients, some claiming 400 year over year growth in revenue run rates as social licenses are spread enterprise-wide. As these companies seek funding to grow in international markets, hire seasoned enterprise sales and account teams and acquire smaller competitors, they’ll need late stage investing over $10m, which bolsters overall valuation before a material event.

Future reports to come: We’ll explore status of top funded investments, which VCs are most active in funding Social Business Software, and other data cuts.

As CEO of one of the 17 self-funded Social Business Software firms, Expion, I™m glad you are delving into the underpinnings of the “why” behind funding.

Personally, it™s good to hear that 31% of the companies in this space

have decided to not go the VC route and I wish it were higher.

I am a serial entrepreneur and agree with your Six Reasons why Startups

Don™t Obtain Investor Funding chart. The only additional point I would add is

the important events for self-funded startups are different than VCs,

and as you know, VC-funded companies tend to focus on different metrics.

For self-started companies using private funding and sweat equity, key

client acquisition and running a profitable business are critical, and

the speed at which you get there “ that is what spells success or

failure. There are lots of companies with cool technologies

and passionate CEOs but if you don’t have a client list of Fortune 500

(or 1000) companies that are buying your product and paying the bills,

you become a ‘hobby’ company that doesn’t last. Specifically, non-funded

companies must innovate faster and have a more agile development

process to incorporate customer requests and continue to exceed client

expectations in order to grow a Fortune 500 client base to keep the cash

flow positive.

Thanks for digging into Social Business Software funding, Jeremiah, and keeping the research fresh.